Try GOLD - Free

CUT YOUR SOCIAL SECURITY

Kiplinger's Personal Finance

|July 2023

Many retirees are dismayed to learn that they owe taxes on a portion of their benefits. But you can take steps to minimize the pain.

After decades of having Social Security taxes withheld from your paycheck, you may not expect to pay taxes on the benefits you've earned. But if you have other sources of income, such as a job, a pension or withdrawals from tax-deferred retirement savings plans, there's a good chance you'll pay taxes on up to 85% of your benefits. Depending on where you live, your state may tax your benefits, too (see the box on page 82).

The government started taxing a portion of Social Security benefits 40 years ago as part of an overhaul designed to shore up the program's finances. Legislation signed by President Ronald Reagan in 1983 imposed taxes on up to 50% of benefits if a retiree's income exceeded specific limits. Ten years later, President Bill Clinton signed legislation that made up to 85% of benefits taxable for retirees whose earnings exceeded a second income threshold.

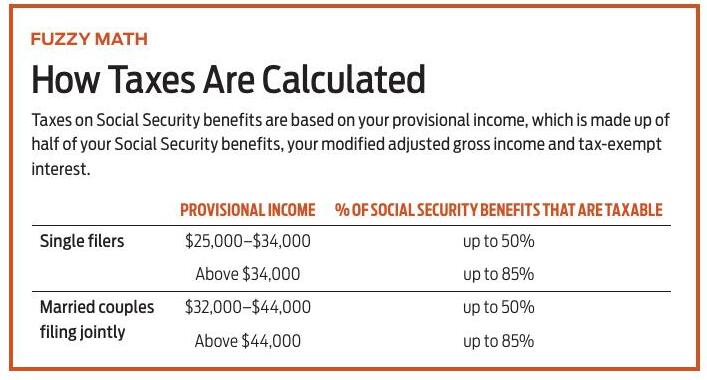

FIGURING THE TAX BITE

The formula is based on what Social Security defines as a beneficiary's provisional income, sometimes referred to as combined income. Your provisional income is based on half of your Social Security benefits, plus other sources that contribute to your adjusted gross income, including wages from a job, withdrawals from traditional tax-deferred accounts, and dividends, interest and capital gains from taxable investment accounts. Interest from municipal bonds, which is generally tax-free, is also included when calculating your provisional income.

If your provisional income ranges from $25,000 to $34,000 for single filers, or $32,000 to $44,000 for joint filers, up to 50% of your benefits will be taxable. If your provisional income is more than $34,000, or $44,000 for joint filers, up to 85% of your benefits will be taxable (see the box below).

This story is from the July 2023 edition of Kiplinger's Personal Finance.

Subscribe to Magzter GOLD to access thousands of curated premium stories, and 10,000+ magazines and newspapers.

Already a subscriber? Sign In

MORE STORIES FROM Kiplinger's Personal Finance

Kiplinger's Personal Finance

Same Story, Different Year

WHAT does the Federal Reserve's rate-reduction initiative mean in the short run for your fixed-income holdings? You'll recall that one year ago, the Fed cut three times, starting by hacking its benchmark overnight funds rate by 0.50 percentage point in September. The year ended with bond markets and fund returns in retreat. It's wishful thinking that cheaper short-term credit and falling money market yields will spark a general bond-buying binge and propel your 2025 total returns toward 10% by year-end.

2 mins

December 2025

Kiplinger's Personal Finance

WHEN HELPING MOM AND DAD HURTS YOUR WALLET

New research shows how assisting an aging parent with expenses can strain your own finances.

3 mins

December 2025

Kiplinger's Personal Finance

WHAT'S AHEAD FOR SOCIAL SECURITY

Bipartisan collaboration on a mix of reforms will likely be needed to keep the system solvent and benefits intact.

3 mins

December 2025

Kiplinger's Personal Finance

WHAT TO MAKE OF A HOT IPO MARKET

This year's crop of initial public offerings could be even dicier than usual because of a skew toward tech and crypto.

5 mins

December 2025

Kiplinger's Personal Finance

Grab a Deal on a Winter Getaway

In the early months of the year, travel demand dips-and so do prices.

5 mins

December 2025

Kiplinger's Personal Finance

8 DIVIDEND FUNDS TO CONSIDER NOW

Our picks deliver a diversified portfolio of dividend stocks.

6 mins

December 2025

Kiplinger's Personal Finance

A NEW WAVE OF ETFS IS ON THE WAY

A long-expected decision from the Securities and Exchange Commission is close to being official, and it could mean more exchange-traded fund options for investors.

1 mins

December 2025

Kiplinger's Personal Finance

CHECKING IN ON THE KIPLINGER DIVIDEND 15

Our favorite dividend payers have had a good year on average, beating the market and yielding twice as much.

14 mins

December 2025

Kiplinger's Personal Finance

THIS FUND FERRETS OUT HIGH-QUALITY STOCKS

THE U.S. stock market has been notching new highs, which tends to kick up the likelihood of a market pullback (defined as a drop of 5% to 10%) or even a correction (a 10% to 20% selloff). That's where JPMorgan U.S. Quality Factor comes in.

1 mins

December 2025

Kiplinger's Personal Finance

New Ways to Use 529 Funds

Tax-free withdrawals from these plans could help you sharpen your job skills.

2 mins

December 2025

Translate

Change font size