Essayer OR - Gratuit

CUT YOUR SOCIAL SECURITY

Kiplinger's Personal Finance

|July 2023

Many retirees are dismayed to learn that they owe taxes on a portion of their benefits. But you can take steps to minimize the pain.

After decades of having Social Security taxes withheld from your paycheck, you may not expect to pay taxes on the benefits you've earned. But if you have other sources of income, such as a job, a pension or withdrawals from tax-deferred retirement savings plans, there's a good chance you'll pay taxes on up to 85% of your benefits. Depending on where you live, your state may tax your benefits, too (see the box on page 82).

The government started taxing a portion of Social Security benefits 40 years ago as part of an overhaul designed to shore up the program's finances. Legislation signed by President Ronald Reagan in 1983 imposed taxes on up to 50% of benefits if a retiree's income exceeded specific limits. Ten years later, President Bill Clinton signed legislation that made up to 85% of benefits taxable for retirees whose earnings exceeded a second income threshold.

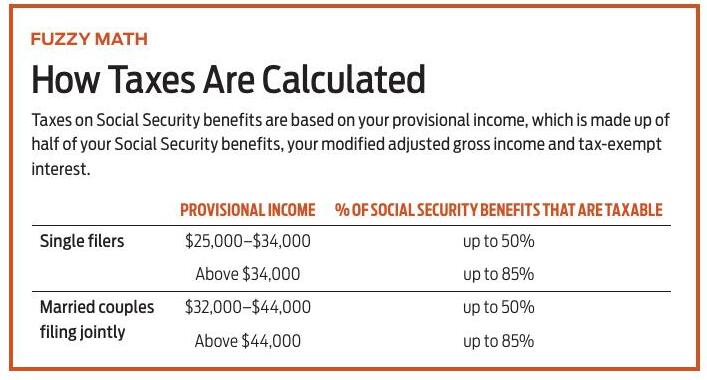

FIGURING THE TAX BITE

The formula is based on what Social Security defines as a beneficiary's provisional income, sometimes referred to as combined income. Your provisional income is based on half of your Social Security benefits, plus other sources that contribute to your adjusted gross income, including wages from a job, withdrawals from traditional tax-deferred accounts, and dividends, interest and capital gains from taxable investment accounts. Interest from municipal bonds, which is generally tax-free, is also included when calculating your provisional income.

If your provisional income ranges from $25,000 to $34,000 for single filers, or $32,000 to $44,000 for joint filers, up to 50% of your benefits will be taxable. If your provisional income is more than $34,000, or $44,000 for joint filers, up to 85% of your benefits will be taxable (see the box below).

Cette histoire est tirée de l'édition July 2023 de Kiplinger's Personal Finance.

Abonnez-vous à Magzter GOLD pour accéder à des milliers d'histoires premium sélectionnées et à plus de 9 000 magazines et journaux.

Déjà abonné ? Se connecter

PLUS D'HISTOIRES DE Kiplinger's Personal Finance

Kiplinger's Personal Finance

IS MONEY MAKING YOU SICK?

Research reveals a strong link between financial well-being and physical and mental health—and what you can do to keep all three in top shape.

12 mins

June 2026

Kiplinger's Personal Finance

THE BEST SMART DEVICES FOR YOUR HOME

These gadgets add comfort and convenience to your living space- and some can even save you money.

5 mins

June 2026

Kiplinger's Personal Finance

Managing the High Cost of Mental Health Care

Cases of anxiety, depression and other conditions are rising, and so is the price of treatment. These strategies can help you get care you can afford.

9 mins

June 2026

Kiplinger's Personal Finance

What This Year's Biggest Medicare Changes Mean for You

Some drug prices are falling, other costs are climbing, and new rules abound. Here's what you need to know.

5 mins

June 2026

Kiplinger's Personal Finance

THE LOWDOWN ON SMARTPHONE INSURANCE

A protection plan can provide peace of mind but may not be worth the cost.

2 mins

June 2026

Kiplinger's Personal Finance

READERS' CHOICE AWARDS 2026

We asked readers to evaluate brokers, wealth managers, credit cards, insurance companies and other financial providers. These are the products and services that stand out from the crowd.

6 mins

June 2026

Kiplinger's Personal Finance

WHERE TO FIND TOP YIELDS

Interest rates are rising along with geopolitical tensions. Pocket yields as high as 13%, depending on your tolerance for risk.

19 mins

June 2026

Kiplinger's Personal Finance

HOW TO HANDLE LOVE AND MONEY THE SECOND TIME AROUND

The financial stakes are higher and the potential pitfalls more plentiful when you say “I do-again.”

10 mins

June 2026

Kiplinger's Personal Finance

A SHIFT AWAY FROM HIGH-TAX STATES

The IRS has released new data on how taxpayers are migrating throughout the U.S., and it reveals a clear pattern: Billions of dollars in income are flowing out of high-tax states and into areas where taxes, and often overall living costs, are lower.

2 mins

June 2026

Kiplinger's Personal Finance

FIGHTING BACK AGAINST INFLATION

INFLATION seems to be going from pesky to pernicious.

1 mins

June 2026

Translate

Change font size