試す 金 - 無料

CIBIL MSME RANK - AN ADDITIONAL DUE DILIGENCE TOOL

BANKING FINANCE

|July 2020

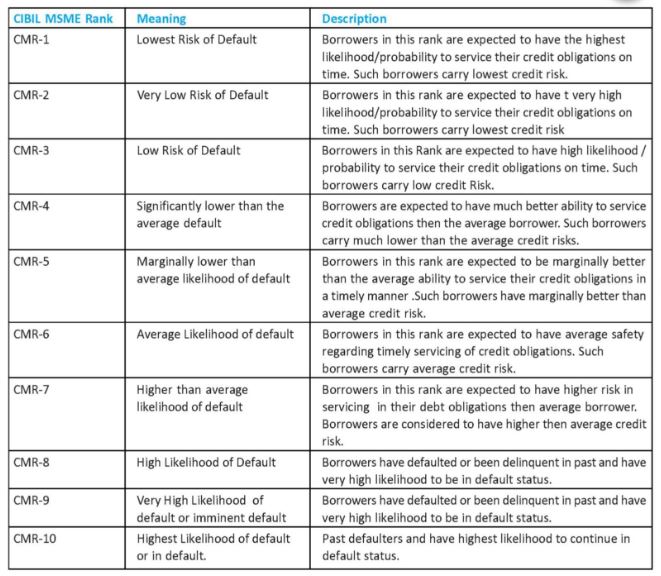

CIBIL MSME Rank is a tool to Access the Credit Risk ranking of Micro, Small and Medium Enterprises to make informed lending decisions, CMR is a credit risk for MSMEs that predicts the probability of an MSME becoming NPA in the next 12 months. It helps us to understand the credit behaviour of MSME as well as the probability of default based on the rank. It is applicable to MSMEs with aggregate commercial borrowing between Rs 10 lakhs to Rs 10 Crores.CMR provides a rank to the MSME based on its credit history data on a scale of 1 to 10.CMR 1 being the best possible rank for the least risky MSMEs and CMR 10 being the riskiest rank for MSMEs.The lower the CMR, the lower the Risk of NPA associated with the MSME.

The Key Parameters used in CMR to measure credit risk are:

1. Liquidity-the liquidity profile of borrower is adjudged by looking at the seasonally adjusted patterns of funds utilization over the past 24 month's period.

2. Firmographics-descriptive attributes like the maturity of the entity, ownership type, industry, location.

3. Repayment Behaviour-month on month analysis of payments made along with the assets classification, are considered to determine if the borrower has a poor or a good track record.

The Model categorises the Entity into broadly three categories:

a) CMR-1 to CMR-3-Never delinquent or No Amount overdue.

b) CMR-4 to CMR-7-Are delinquent but never an NPA

c) CMR-8 to CMR-10-are known to be NPA at some point in time in the past 24 months.

Important points:

1. Borrowers with CMR rating up to CMR-3 should be given preference for faster disposal

2. For CMR 4/5, need-based facilities may be approved.

3. For CMR 6/7, Proper justification for the sanction/enhancement should be given. Credit Risk mitigants like additional collateral, guarantee etc.may be stipulated.

このストーリーは、BANKING FINANCE の July 2020 版からのものです。

Magzter GOLD を購読すると、厳選された何千ものプレミアム記事や、10,000 以上の雑誌や新聞にアクセスできます。

すでに購読者ですか? サインイン

BANKING FINANCE からのその他のストーリー

BANKING FINANCE

Ravi Ranjan appointed SBI managing director, to oversee risk and stressed assets

State Bank of India (SBI) has appointed Ravi Ranjan as its Managing Director with effect from December 15, 2025, according to a regulatory filing by the country's largest public sector lender.

1 min

January 2026

BANKING FINANCE

Reserve Bank News

Reserve Bank of India has appointed Usha Janakiraman as Executive Director with effect from December 1, 2025, according to an official release issued by the central bank. Her appointment comes just days ahead of the Monetary Policy Committee (MPC) meeting scheduled for December 3.

7 mins

January 2026

BANKING FINANCE

Mutual Fund News

Children's mutual funds, once a niche investment option, are increasingly becoming a mainstream tool for long-term financial planning in Indian households, especially for education-related goals.

7 mins

January 2026

BANKING FINANCE

Co-Operative Bank News

As per the Reserve Bank of India's Report on Trend and Progress of Banking in India 2024-25, State Cooperative Banks (StCBs) and District Central Cooperative Banks (DCCBs), which together constitute the short-term rural cooperative credit structure, reported steady balance sheet expansion, sustained growth in deposits and advances, and improving asset quality during 2024-25.

2 mins

January 2026

BANKING FINANCE

Legal News

Foreign firms can't claim full deduction for head of- fice expenses on Indian biz: SC

5 mins

January 2026

BANKING FINANCE

Banks unlikely to cut deposit and MCLR rates despite RBI repo rate reduction

Despite the Reserve Bank of India delivering a 25 basis points cut in the repo rate last week, banks are unlikely to reduce term deposit rates or marginal cost of funds-based lending rates (MCLR) aggressively, according to senior bankers.

1 min

January 2026

BANKING FINANCE

The Race for the Super App: Will India's BFSI Ecosystem Converge?

The concept of a Super App has its roots primarily in Asia. The term is often credited to refer to platforms that began with one core function (messaging, ride-hailing, payments) and then expanded to offer a portfolio of services accessed through the same interface. For example, WeChat in China began as a messaging app and evolved into payments, e-commerce, ride-hailing, mini-programs and more.

10 mins

January 2026

BANKING FINANCE

Government to divest up to 3% stake in Indian Overseas Bank via OFS

Shares of Indian Overseas Bank (IOB) came under selling pressure after the Government of India announced plans to divest up to 3% of its equity through an Offer for Sale (OFS).

1 min

January 2026

BANKING FINANCE

Unclaimed bank deposits in India more than double in five years

India's unclaimed bank deposits have more than doubled over the past five years, rising to Rs. 67,004 crore as on June 30, 2025, from Rs. 27,824 crore at the end of FY21, highlighting a growing challenge for the banking system.

1 min

January 2026

BANKING FINANCE

Cyber Insurance: Safeguarding Businesses in the Age of Digital Transformation

Cyber insurance, also known as cyber liability insurance or cyber risk insurance, is a specialized form of coverage designed to protect businesses from internet-based risks and more generally from risks relating to information technology infrastructure and activities.

8 mins

January 2026

Translate

Change font size