Poging GOUD - Vrij

GET THE RIGHT ADVICE IN RETIREMENT

Kiplinger's Personal Finance

|February 2025

If you've saved up a decent-size nest egg with a financial services firm, chances are good it has offered you financial advice-for a price. Is it worth it?

IF you're approaching retirement or have already stopped working, it may have occurred to you that saving for retirement was the easy part.

Most likely, you had contributions to a 401(k) or other employer-provided retirement savings account automatically deducted from your paycheck. Target-date funds, which automatically adjust your investments as you approach retirement, have taken the guesswork (and hopefully the stress) out of investing those contributions. For investments outside of your workplace plan, many brokerage firms have harnessed digital tools to provide low-cost investment advice. (For our evaluation of the online services that many major brokers provide, see "Ranking the Online Brokers," Oct.) But once you retire and need to start withdrawing from your nest egg, the task of managing your money becomes more difficult. Fewer than half of retirees say they've estimated how much they'll need to withdraw from their savings and investments to cover their expenses, according to the Employee Benefit Research Institute's 2024 Retirement Confidence Survey.

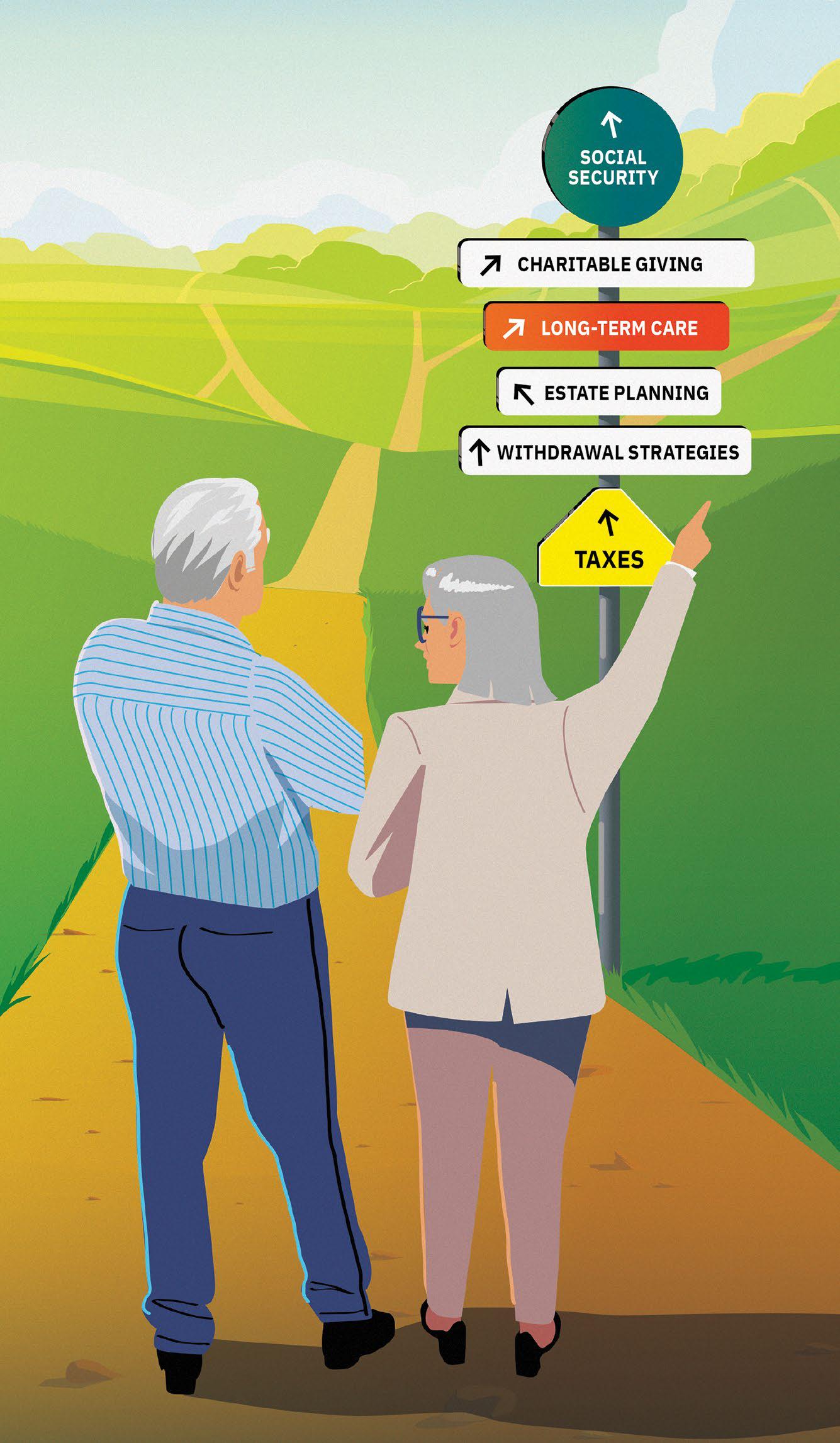

Even if you've nailed down the amount of income you'll need each month to retire comfortably, you'll have to wrestle with a host of decisions that can't be put on autopilot, such as which accounts you should tap first, how to lower taxes on your withdrawals and when you should sign up for Social Security. Add to the mix concerns about long-term care, estate planning and charitable giving, and you may start to feel as though managing your savings is a full-time job.

Even if you've nailed down the amount of income you'll need each month to retire comfortably, you'll have to wrestle with a host of decisions that can't be put on autopilot, such as which accounts you should tap first, how to lower taxes on your withdrawals and when you should sign up for Social Security. Add to the mix concerns about long-term care, estate planning and charitable giving, and you may start to feel as though managing your savings is a full-time job.With the stakes so high, you're probably going to want some advice.

Dit verhaal komt uit de February 2025-editie van Kiplinger's Personal Finance.

Abonneer u op Magzter GOLD voor toegang tot duizenden zorgvuldig samengestelde premiumverhalen en meer dan 9000 tijdschriften en kranten.

Bent u al abonnee? Aanmelden

MEER VERHALEN VAN Kiplinger's Personal Finance

Kiplinger's Personal Finance

A TAX BREAK FOR MEDICAL EXPENSES

The editor of The Kiplinger Tax Letter responds to readers asking about health care write-offs.

2 mins

February 2026

Kiplinger's Personal Finance

Volunteering to Help Others at Tax Time

Through an IRS program, qualifying individuals can get free assistance with their tax returns.

2 mins

February 2026

CHANGE")

Kiplinger's Personal Finance

CATCH-UP SAVERS FACE A TAXING 401(K) CHANGE

Under new rules, you may lose an up-front deduction but gain tax-free income once you retire.

2 mins

February 2026

Kiplinger's Personal Finance

The Case for Emerging Markets

Economic growth, earnings acceleration and bargain prices favor EM stocks.

3 mins

February 2026

Kiplinger's Personal Finance

THE NEW RULES OF RETIREMENT

Popular guidelines about how to save, invest and spend need to be updated and personalized to ensure you'll never run out of money.

15 mins

February 2026

Kiplinger's Personal Finance

Smart Ways to Share a Credit Card

Adding an authorized user has its benefits, but make sure you set the ground rules.

2 mins

February 2026

Kiplinger's Personal Finance

THE BEST AFFORDABLE FITNESS TRACKERS

These devices monitor your exercise, sleep patterns and more- and they don't cost an arm and a leg.

4 mins

February 2026

Kiplinger's Personal Finance

A VALUE FOCUS CLIPS RETURNS

THERE'S more to Mairs & Power Growth than its name implies. The managers favor firms with above-average earnings growth. But a durable, competitive position in their market- “a number-one or number-two position and gaining share,” says comanager Andrew Adams—and a reasonable stock price matter even more.

1 mins

February 2026

Kiplinger's Personal Finance

Look Beyond the Tech Giants

I am hooked on a podcast called Acquired, in which two smart guys do a deep analytical dive, typically lasting three or four hours, on a single successful company such as Coca-Cola or Trader Joe's. Ben Gilbert and David Rosenthal, a pair of venture capitalists, are especially adept at explaining what's behind the success of such tech giants as Alphabet (symbol GOOGL, $320), the former Google, which recently merited 11 hours and 42 minutes of dialogue all by itself.

4 mins

February 2026

Kiplinger's Personal Finance

How to Pay for Long-Term Care

A couple of months ago, I wrote that many Americans significantly underestimate how long they could live in retirement (see “Living in Retirement,” Dec.). With the possibility of a 30-year retirement becoming more common, retirees need to plan for so-called longevity risk to make sure their assets last a lifetime. And the longer you live, the more likely you'll need to pay for some form of long-term care. That can range from assistance with activities of daily living to in-home care to a nursing home stay.

2 mins

February 2026

Listen

Translate

Change font size